Political Risk Insurance Calculator

Calculate Your Political Risk Coverage

When your company invests millions in a mine in the Democratic Republic of Congo, a power plant in Egypt, or a manufacturing hub in Vietnam, you’re not just betting on markets-you’re betting on governments staying stable, laws staying consistent, and borders staying open. But what happens when a military coup freezes foreign assets? Or a new president nationalizes your equipment? Or the currency suddenly can’t be converted to dollars? This is where political risk insurance stops being a luxury and becomes a survival tool.

What Political Risk Insurance Actually Covers

Political risk insurance (PRI) isn’t just another line on your corporate insurance policy. It’s a targeted shield against government-driven disasters that standard commercial policies won’t touch. Think of it as insurance for when the state itself becomes the threat. The core coverages are clear and brutal in their specificity:- Expropriation, nationalization, or confiscation - When a government seizes your assets without fair compensation. This isn’t a tax hike. It’s a takeover.

- Currency inconvertibility or non-transfer - You make profits in local currency, but the government blocks you from converting or moving it out. No cash flow. No exit.

- Political violence - War, terrorism, riots, sabotage. Not just damage to property, but the complete collapse of operational safety.

- Contract frustration or non-honoring - The government cancels your license, breaks a signed agreement, or refuses to enforce your contract. Even if you did everything right.

- Forced divestiture or deprivation of capital - You’re forced to sell your stake at fire-sale prices, or your capital is locked up indefinitely.

Private vs. Public Providers: Who’s Really Backing You?

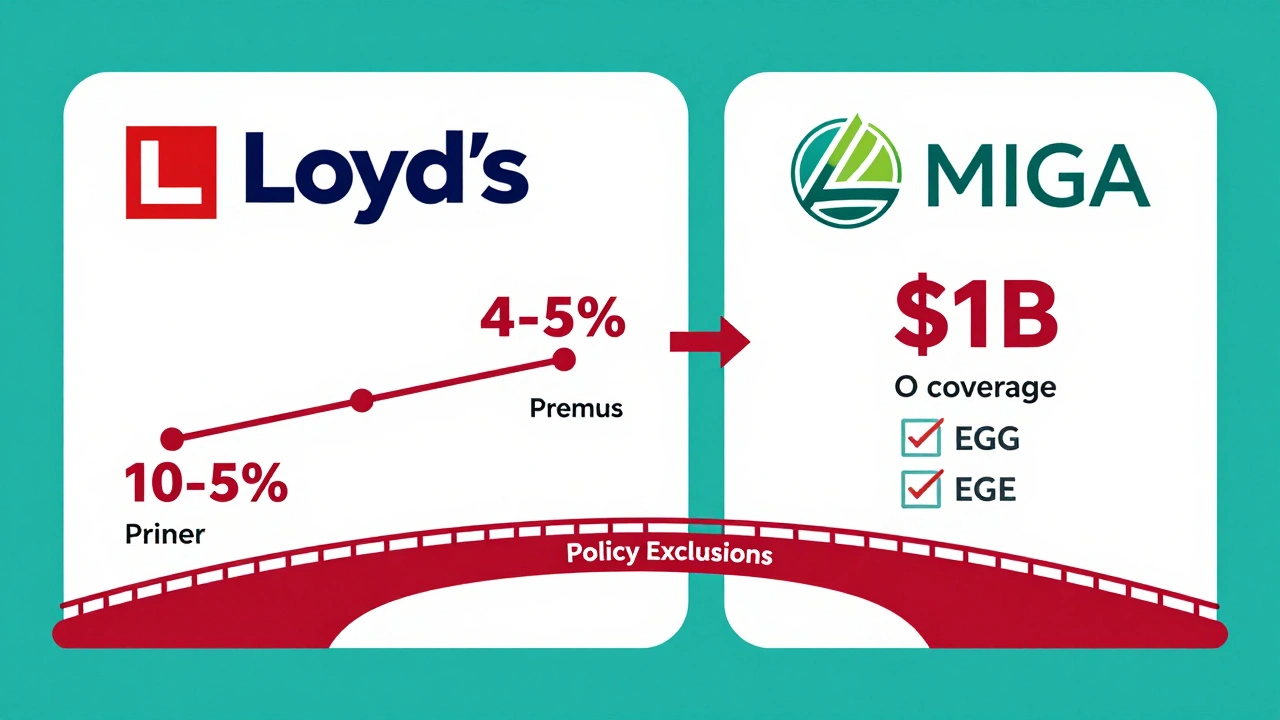

Not all political risk insurance is created equal. You’ve got two main paths: private insurers and public agencies. Private insurers - like Lloyd’s of London, AIG, Starr Insurance, Euler Hermes - move fast. Underwriting takes 4 to 6 weeks. They’ll write policies from $5 million up to $500 million. But they cap terms at 5 years. Premiums? Between 0.5% and 5% of the insured value. In high-risk countries like Iran or Venezuela, you’re looking at 4-5% annually. That’s expensive, but it’s flexible. Public providers - the U.S. DFC, MIGA (World Bank), and national export credit agencies - are slower. It takes 8 to 12 weeks to get a policy. But they can insure up to $1 billion and offer terms up to 15-20 years. Their premiums are often half of what private insurers charge. Why? Because they’re backed by governments. They can afford to take longer-term bets. But here’s the catch: public insurers don’t just assess risk. They assess your behavior. The U.S. DFC requires compliance with environmental standards like the Equator Principles. MIGA demands social impact reviews. If your project doesn’t meet their ESG benchmarks, you get denied - even if the political risk is high.Why 63% of Companies in High-Risk Countries Now Buy It

Five years ago, only 41% of companies operating in volatile markets bought political risk insurance. Today, it’s 63%. Why the jump? Because the risks are no longer rare. They’re routine. The PRS Group’s 2025 Political Risk Yearbook shows global geopolitical risk has risen 22% since 2020. The Middle East, Sub-Saharan Africa, and Latin America are now hotspots. In 2024, a construction firm in Egypt lost a $50 million claim because their license was canceled over a vague clause about “failure to demonstrate force majeure.” The policy wording was so dense, they didn’t realize the trigger was buried in a footnote. Companies that have been burned before don’t make that mistake twice. According to Willis Towers Watson, firms that’ve suffered a political loss are 2.3 times more likely to keep their PRI coverage. And it’s not just mining or energy. Manufacturing is catching up - 43% now have coverage, up from 28% in 2020. Why? Because of US-China trade tensions. Fifty-four percent of manufacturers are expanding PRI coverage for operations in China, fearing sudden export bans or forced tech transfers.

The Hidden Gaps: What’s Not Covered (And Why You’ll Get Denied)

PRI sounds like a safety net. But it’s full of holes. The biggest trap? “General regulatory changes.” If a government raises tariffs, introduces new environmental rules, or imposes broad export controls - that’s usually excluded. It’s not “political risk.” It’s just “policy.” You’re expected to absorb that. Currency claims are the most frequently denied. Jardine Lloyd Thompson’s 2024 claims report found 43% of currency inconvertibility claims get rejected. Why? Because insurers demand proof the restriction was politically motivated - not just a result of economic collapse. Proving intent is nearly impossible. Another blind spot? Cyberattacks with political motives. In 2025, Chubb’s Chief Political Risk Officer confirmed 37% of recent claims involved cyber incidents tied to state actors - like hackers shutting down a mine’s control systems during a coup. Most PRI policies didn’t cover this until January 2025, when the U.S. DFC launched its new Cyber Political Risk product. Companies without that upgrade are exposed.How to Get It Right: A Realistic 6-Step Process

Getting political risk insurance isn’t like buying office insurance. It’s a complex negotiation. Here’s how to do it without getting screwed:- Map your exposure - List every asset, contract, and operation in high-risk countries. Don’t skip the intangible ones - licenses, permits, supply chain agreements.

- Check country risk scores - Use World Bank CPIA scores, EIU Country Risk Service, or Verisk Maplecroft. Don’t guess. Data drives pricing.

- Choose your insurer type - Need speed and flexibility? Go private. Need long-term, large-scale coverage? Go public. Don’t mix them unless you’re a Fortune 500.

- Get a broker - Use Marsh or Willis Towers Watson’s specialty political risk teams. They know the fine print and how to negotiate exclusions.

- Read the policy like a lawyer - Pay attention to waiting periods (30-180 days for currency claims), causation requirements, and definitions of “political event.” If it’s vague, demand clarity.

- Document everything - Keep records of government communications, financial flows, and operational logs. Claims are won or lost on paper trails.

What’s Next? The Future of Political Risk Insurance

The market is evolving fast. In 2024, MIGA started offering climate-resilient PRI policies - tying political risk coverage to environmental adaptation plans. That’s new. And it’s becoming standard. ESG is now baked into underwriting. Eighty-two percent of insurers adjust premiums based on a company’s ESG performance. Poor labor practices? Higher premiums. Strong community engagement? Lower rates. The next frontier? Hybrid threats. AIG is piloting a product that covers coordinated cyber-physical attacks - like hackers disabling a dam’s controls during a protest. That’s not just political risk. It’s a new kind of warfare. And then there’s AI disinformation. A 2025 J.S. Held survey found 73% of insurers admit they don’t cover losses from AI-driven campaigns that trigger public outrage, boycotts, or government crackdowns. That’s the next $100 million gap.Final Reality Check

Political risk insurance doesn’t eliminate risk. It just gives you a financial backstop when the unthinkable happens. It won’t stop a coup. It won’t restore your license. But it will give you cash to walk away - and rebuild elsewhere. If you’re investing in places where governments change hands violently, laws shift overnight, or currencies freeze - you’re not being paranoid. You’re being strategic. The companies that survive global volatility aren’t the ones that avoid risk. They’re the ones that priced it, insured it, and planned for it.What’s the difference between political risk insurance and terrorism insurance?

Terrorism insurance only covers attacks that meet a legal definition of terrorism - usually by non-state actors. Political risk insurance covers government actions like expropriation, currency controls, and contract cancellations - things terrorism insurance won’t touch. You need both if you’re in a high-risk area.

Can I get political risk insurance for a startup?

Yes, but it’s harder. Private insurers usually require proven assets and revenue. Startups often need to partner with a larger parent company or use public providers like MIGA, which sometimes insure early-stage projects tied to development goals. Be ready to show a detailed business plan and risk mitigation strategy.

How long does a claim take to pay out?

On average, 6 to 12 months. Public providers like MIGA can take longer due to bureaucratic reviews. Private insurers may pay faster - but often fight claims harder. Documentation quality is the biggest factor in speed. Companies with clean, real-time records get paid quicker.

Is political risk insurance worth the cost?

If you’re investing more than $10 million in a politically unstable country, yes. The average claim size is $89 million (J.S. Held, 2024). Premiums are 0.5%-5% of that. That’s a small price to avoid losing everything. For smaller investments, consider joint ventures with local partners or political risk clauses in contracts.

Do I need political risk insurance if I’m just exporting goods?

If you’re shipping to a country with currency controls or a history of import bans, yes. Even exporters face non-payment risk if a government freezes foreign exchange. Many export credit agencies offer short-term political risk coverage as part of their trade finance packages.

Can I cancel my political risk insurance policy early?

Usually not without penalty. Policies are structured for the full term. But some private insurers allow partial refunds if you sell your asset or exit the country. Always check the cancellation clause before signing.