Retirement Age Calculator

Understand Your Retirement Options

See how retirement age reforms might impact your pension based on your current situation.

Your Retirement Outlook

Adjusted Retirement Age:

Pension Impact:

Years Until Retirement:

--

--

--

Based on global trends showing retirement ages rising by 1 year for every 2 years of increased life expectancy.

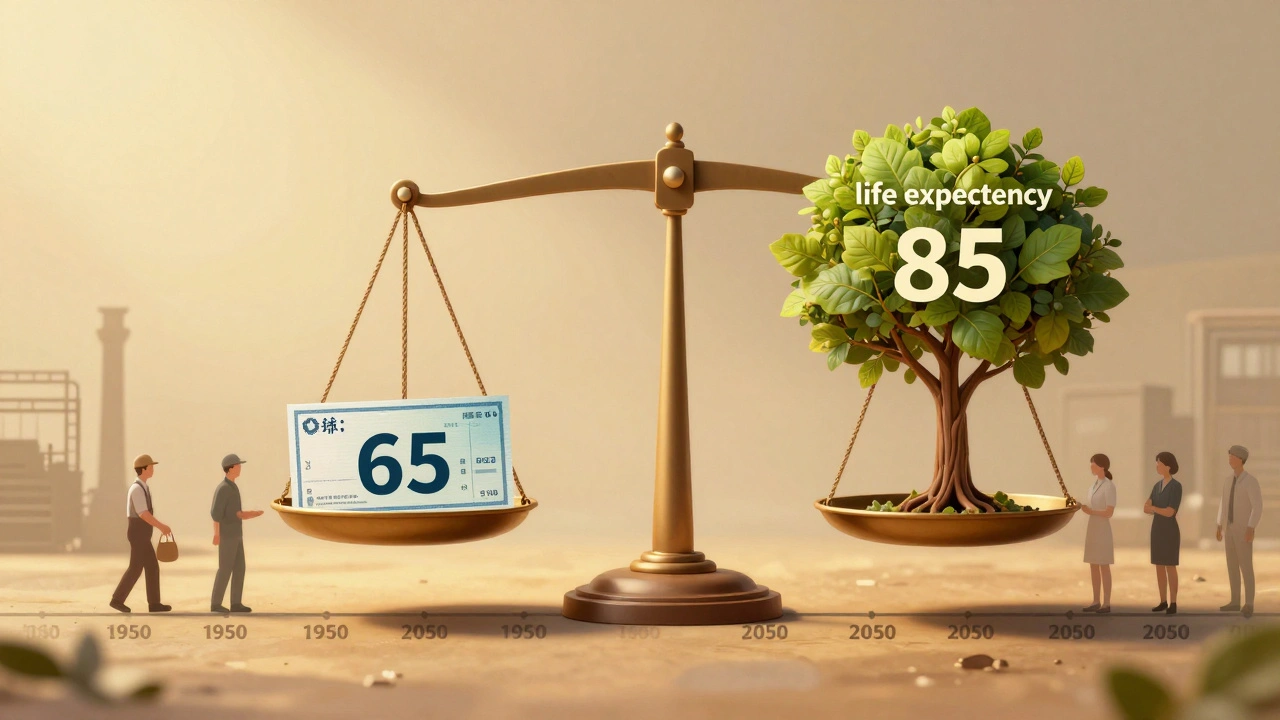

People are living longer. But the retirement age hasn’t kept up.

By 2050, more than 1.6 billion people will be over 65. That’s more than double today’s number. Meanwhile, fewer babies are being born. In 1990, the global fertility rate was 3.2 children per woman. Today, it’s 2.4. This isn’t a future problem-it’s happening right now. Governments are scrambling to fix pension systems that were built for a world that no longer exists.

For decades, most countries set retirement ages at 60, 62, or 65 based on life expectancies from the 1950s. Back then, few people lived past 70. Now, the average person in a high-income country lives into their late 80s. That means someone who retires at 65 might collect a pension for 25 years. That’s not sustainable. And it’s not fair to younger workers who will pay for it.

Why retirement age reforms are happening now

The 2008 financial crisis was a wake-up call. Countries saw their pension funds shrink as markets crashed, while the number of retirees kept growing. The OECD found that since 2010, more than half of its member countries have raised the official retirement age. Denmark is planning to raise it to 70 by 2040-and possibly 74 by 2060. Italy is targeting 71 by 2060. Even China, which had one of the lowest retirement ages in the world, is raising it by 3 to 5 years for men and women by 2039.

These aren’t random decisions. They’re math. When life expectancy goes up by one year, countries like Finland and Italy automatically add several months to the retirement age. That’s called indexing. The Netherlands does it too. It’s not political-it’s algorithmic. The goal? Keep the system balanced. If people live longer, they work longer-or get less money per year.

But here’s the catch: not everyone can work longer. A factory worker with arthritic knees can’t just “keep going.” A nurse on her feet all day can’t wait until 70. That’s why flexible models are gaining ground. Norway and Finland let people retire anytime between 62 and 75, but if you take your pension early, it’s reduced. If you wait, you get more. Sweden lets people work part-time and collect a partial pension from 61. That’s not just fair-it’s practical.

Who’s working longer-and who’s not

Between 2000 and 2024, employment among people aged 45 to 64 rose by 9.3 percentage points across OECD countries. But that number hides big differences. In Sweden, Denmark, and Norway, over 75% of people aged 60 to 64 are still working. In Italy, Greece, and Spain, it’s below 50%. Why? Culture matters, but so do policies. Countries with rigid retirement rules see people drop out early. Countries with flexible options keep them in the workforce.

Japan’s approach is telling. Instead of forcing people to work longer, they offer higher pensions for those who delay retirement past 65. They also run “Silver Human Resource Centers” that connect seniors with part-time jobs. In the Netherlands, workers can reduce hours while drawing part of their pension. These aren’t perks-they’re solutions.

In the U.S., the State Street Global Advisors 2025 Retirement Reality Report found that 33% of workers now plan to retire later than they originally thought. Thirty percent plan partial retirement. Only 8% plan to retire before 65-down from 16% just a year earlier. Younger workers are less optimistic than ever. One Reddit user wrote: “I planned to retire at 62 based on government materials from 2010. Now I’m being told I need to work until 67 just to get the same benefits.”

The political cost of change

Here’s the hardest part: people hate it when their retirement age goes up. France’s 2023 reform-raising the age from 62 to 64-sparked nationwide protests. President Macron had to use emergency powers to push it through. In Mauritius, a proposal to raise the retirement age from 60 to 65 met immediate union resistance. Brazil’s 2019 reform was a political earthquake. Even in countries where the reform was technically sound, the backlash was fierce.

Why? Because retirement isn’t just a number. It’s a promise. People plan their lives around it. They buy houses, send kids to college, save for travel-all based on the assumption they’ll stop working at 60, 62, or 65. When that promise changes, it feels like betrayal.

But here’s what most people don’t realize: the alternative is worse. If retirement ages stay the same, either pensions get cut across the board, or younger workers pay higher taxes to support retirees. Neither option is popular. But one is inevitable.

What works-and what doesn’t

Successful reforms don’t just raise the age. They add flexibility. They communicate clearly. They include support for older workers.

Take Singapore. They raised the retirement age from 63 to 65 by 2030-but also raised the re-employment age to 70. That means companies must offer jobs to workers up to 70. They’re not forced to keep them, but they must offer the chance. That’s smart. It gives people choice.

Canada’s enhanced Canada Pension Plan lets people start collecting between 60 and 70, with payments adjusted actuarially. Start at 60? You get less each month. Wait until 70? You get more. No one’s forced to work longer, but the system rewards those who do.

Meanwhile, countries that just raise the age without support-like Romania and Bulgaria, which are bringing retirement to 65 for both men and women-see little change in workforce participation. People don’t have the option to work longer, so they don’t. They just wait for their pension, even if it’s smaller.

And then there’s India. Despite fiscal pressure, the government has refused to raise the retirement age from 60. Why? Because over 90% of workers are in the informal sector-street vendors, domestic workers, day laborers. They don’t get pensions anyway. Raising the age wouldn’t help them. It would just hurt the few who do have formal jobs.

What’s next? The global picture by 2040

The World Economic Forum predicts the global average retirement age will hit 67.5 by 2040. High-income countries will be at 68.7. Low-income countries? Still below 62. That gap matters. It means retirees in rich countries will live longer, healthier lives-and have pensions to match. In poorer countries, people will keep working out of necessity, not choice.

That’s the real challenge: equity. A woman in rural Bangladesh doesn’t have the same options as a man in Oslo. Reform isn’t just about math. It’s about justice.

Experts agree: the best reforms combine three things-gradual increases, flexible options, and better financial education. People need to understand that their pension isn’t a fixed gift. It’s a shared system. And if they live longer, they need to plan for it.

Sweden’s partial pension model is popular for a reason. It lets people ease into retirement. They work fewer hours. They earn less. But they still get part of their pension. That reduces stress. It keeps skills in the economy. It gives people dignity.

What you can do now

Even if your country hasn’t changed the rules yet, the trend is clear. Don’t rely on a 65 retirement. Start planning for 70.

- Save more. If you expect to work longer, save less for the early years and more for the later ones.

- Invest in your health. If you can’t work because of physical strain, no pension will help.

- Learn new skills. The jobs of 2035 won’t be the same as today. Adaptability matters.

- Ask your employer about phased retirement. Many companies don’t advertise it-but they’ll offer it if you ask.

The system is changing. You can wait for it to hit you-or you can prepare for it.

Why are retirement ages going up?

Retirement ages are rising because people are living longer and having fewer children. When more people live past 80 and fewer workers are paying into the system, pensions become unsustainable. Governments are adjusting the retirement age to match life expectancy and keep the system financially balanced.

Does raising the retirement age mean I have to work until 70?

Not necessarily. Many countries now offer flexible options-you can retire earlier but get less money, or delay retirement and get more. Some allow part-time work with partial pensions. The goal isn’t to force everyone to work until 70, but to give people choices that match their health, job, and financial needs.

What if I work in a physically demanding job?

That’s a major concern. Reforms must include protections for workers in manual labor, healthcare, or other physically taxing roles. Some countries allow early retirement with reduced penalties for these workers. Others offer retraining or lighter duties. Without these accommodations, raising the retirement age just pushes vulnerable people into hardship.

Why don’t all countries raise the retirement age?

Many low- and middle-income countries don’t have formal pension systems at all. Over half the world’s workforce is in the informal economy-street vendors, farm workers, domestic helpers-who don’t pay into pensions. For them, raising the retirement age doesn’t change anything. Their challenge isn’t pension reform-it’s building a system that includes them.

Will my pension be cut if I retire early?

Yes, in most countries with modern systems. If you retire before the official age, your pension is reduced to account for the longer payout period. For example, retiring at 60 instead of 67 might mean a 30-40% lower monthly payment. But if you wait until 70, your payment could be 20-30% higher. It’s an actuarial trade-off-longer life means smaller payments if you start early.

How do I know what my retirement age will be?

Check your country’s official pension website. Many now use automatic indexing based on life expectancy, so your retirement age depends on your birth year. If you were born after 1970, you’ll likely retire at 67 or later. Use online calculators from your national pension agency-they’ll give you your exact age based on your birth date and current laws.

What happens if we don’t act?

If no reforms happen, pension systems will collapse under the weight of aging populations. The European Commission estimates public pension spending could rise by 1.8% of GDP by 2070-meaning higher taxes, deeper cuts, or both. That’s not speculation. It’s projection.

And the cost isn’t just financial. When people can’t retire on time, they delay starting families. They skip medical care. They live in fear. That’s the hidden toll of inaction.

The answer isn’t to keep pretending we can retire at 60 forever. It’s to build a system that works for longer lives-and respects the dignity of every worker, no matter their job or income.